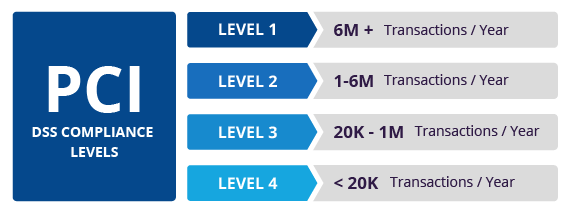

Why PCI Standards Matter

In my experience, PCI Standards matter because payment card information is one of the most frequently targeted forms of sensitive data. If an organization handles cardholder data carelessly, the consequences can include fraud losses, reputational damage, regulatory scrutiny, contractual penalties, and loss of customer confidence. Strong payment security is therefore not optional. It is fundamental to doing business responsibly.

This is especially important because payment ecosystems often involve multiple systems and third parties. Merchants, service providers, payment gateways, software platforms, and infrastructure environments may all play a role in the transaction flow. Without clear standards, it becomes much easier for gaps in configuration, access control, or monitoring to expose sensitive information.

There is also a strong connection to security Knowledge here. Understanding PCI means understanding how technical controls, operational processes, and shared responsibility work together to protect financial data.

My Perspective on Payment Card Security

What changed my understanding of PCI Standards was realizing that compliance alone does not automatically equal security. At first, it is easy to see PCI as a checklist to complete for audits or contractual obligations. But over time, I came to see that the most effective organizations treat PCI as a baseline rather than an endpoint. The standard establishes important controls, but true resilience depends on whether those controls are actively maintained, tested, and integrated into daily operations.

That matters because attackers do not care whether a business once passed an assessment. They care about weaknesses that exist now. A secure payment environment requires more than documented policies. It requires disciplined implementation, visibility, and continuous attention.

Key Components of PCI Standards

I think PCI Standards become easier to understand when the main control areas are broken down clearly.

Protecting cardholder data

Sensitive payment data must be stored and transmitted securely.

Access control

Only authorized individuals should be able to access systems and data related to payment processing.

Network security

Firewalls, segmentation, and secure configurations help reduce exposure.

Monitoring and logging

Organizations need visibility into system activity and suspicious behavior.

Vulnerability management

Systems must be patched, tested, and protected against known weaknesses.

Security policy and governance

Procedures, responsibilities, and staff awareness all support effective implementation.

Common Challenges in PCI Standards Implementation

I have noticed that organizations often struggle with PCI Standards in a few recurring ways.

Overly broad scope

If payment environments are not segmented properly, compliance scope becomes harder to manage.

Weak access hygiene

Shared accounts, excessive privileges, and poor authentication increase risk.

Inconsistent patching

Unpatched systems remain one of the easiest ways for attackers to gain entry.

Limited visibility

Without proper logging and monitoring, suspicious activity may go undetected.

Treating compliance as periodic

Security weakens quickly when controls are only reviewed near assessment time.

Practical Ways to Strengthen PCI Standards Compliance

I believe PCI Standards are most effective when organizations combine compliance discipline with real operational security.

Reduce the card data footprint

Store, process, and transmit only what is truly necessary.

Segment payment systems

Separate cardholder data environments from broader business networks where possible.

Enforce strong authentication

Use unique accounts, strong passwords, and multi-factor authentication where applicable.

Monitor continuously

Review logs, alerts, and anomalies as an ongoing security practice.

Test and improve regularly

Vulnerability scans, penetration testing, and control reviews should be part of routine operations.

Below is a simple overview of the framework:

| PCI Control Area |

Why It Matters |

Example in Practice |

| Data protection |

Secures cardholder information |

Encrypting data in transit and at rest |

| Access control |

Limits unnecessary exposure |

Restricting payment system access by role |

| Network security |

Reduces attack surface |

Using firewalls and segmentation |

| Monitoring |

Detects misuse or intrusion |

Logging payment system activity |

| Vulnerability management |

Prevents exploitation |

Applying patches and running security scans |

These elements show that PCI is not a single safeguard. It is a layered security model built around payment risk reduction.

Why PCI Standards Matter Beyond Compliance

I think PCI Standards matter because they influence how customers judge the reliability of digital commerce. Most users do not see the technical architecture behind a transaction, but they do feel the consequences when something goes wrong. A payment breach can damage trust faster than almost any other type of incident.

That is why PCI matters beyond audits and contracts. It supports the credibility of online business itself. Strong card security helps protect revenue, brand reputation, customer relationships, and the wider confidence that keeps digital payments functioning at scale.

Final Thoughts

For me, PCI Standards represent one of the clearest examples of practical cybersecurity in action. They turn the broad goal of payment protection into a structured set of safeguards that organizations can implement, measure, and improve over time.

That is why they remain essential. In a world where digital payments are routine, securing cardholder data is not just a compliance task. It is a core responsibility of modern business.

Explore our “Technology” category for more insightful content!

Don't forget to check out our previous article: ETL Processes: Designing Robust Pipelines for Data Ingestion and Transformation